Weekly Risk Radar

Top Takeaways

Small Print? Reddit. We'll leave last week's "David versus Goliath" storytelling to the journalists. It's not that the story doesn't matter. It does. The week of January 25, 2021 may prove to be one of those seminal moments in the global capital markets' long timeline, like "The Big Short" (2007-08) or the bailout of Long Term Capital Management (1998). Last week's events provide more evidence that markets are broken. Retail investors learned a hard lesson about margin calls. Prime brokers, the firms that finance and enable short-selling by speculators, hedge funds, and risk managers, are said to have had their largest gross exposure drawdowns, an 8-standard deviation event. There's not a page in the risk management playbook for what happened last week. Maybe there should be. What did we learn? (1) know your liquidity, (2) asymmetrical risk exists in markets and in social media, (3) always read the fine print. The fallout from last week's events won't be on full display until the end of the first quarter.

Why it matters (1). $3.7 trillion in global market capitalization was destroyed last week, equal to the GDP of Germany.

Why it matters (2). The VIX spiked to 37 and closed the week at 33. Nothing good happens when the VIX is greater than 30. A defining characteristic of the stock market during the pandemic is structurally higher volatility. For example, the VIX's 200-day moving average has not traded below 20 since April 2020, well above its seven-year average of 15. At these VIX levels, the risk management divisions of asset management firms are in charge. Winners are sold to cover losers. Portfolio managers "get small" by reducing their total risk allocations.

Plugged in. General Motors announced that it would stop making gas-powered vehicles and produce only electric passenger and SUV vehicles by 2035. Is this a buy the rumor, sell the news moment? According to one infamous sell-side shop, electric vehicle (EV) and solar power stock performance fit the historical profile of an asset bubble, likening the stock price action over the last year to the Nikkei in 1989, Nasdaq in 2000, and commodities in 2008. In those historical examples, prices quadrupled over a span of three years. By comparison, EV stocks have increased 10-fold in the past three years.

Cycle analysis

Liquidity cycle (80% of factors are favorable). Global liquidity remains accommodative; however, the global money supply is growing at a six-month rate of change of 7.9% (down from 8.6%), and U.S. commercial bank lending is 14% below its peak set last May. The top six global central banks' cumulative assets have declined by 1% since the beginning of the year in USD-terms. Only the Fed and the Bank of England have expanded liquidity in 2021. Based on Fed guidance, we expect the Fed's balance sheet to grow from $7.4 trillion to $9.0 trillion (45% of US GDP) by the end of 2021.

Business cycle (47% of factors are favorable). A steeper yield curve, rising bond yields, and outperformance of commodities infer we are in a reflationary economic regime. The Conference Board's U.S. Leading Economic Index was less bad, rising from -2.2% to -1.7%.

Market cycle (38% of factors are favorable). The VIX Index is trading above 30, signaling stocks are in a risk-off mood. Three of our five proprietary risk trend models are flashing risk-off. The market sentiment pendulum has corrected from greedy to fearful. The CNN Fear & Greed Index is now at 37 (it was 60 one week ago). Overly bullish sentiment is no longer a headwind.

Monthly recap

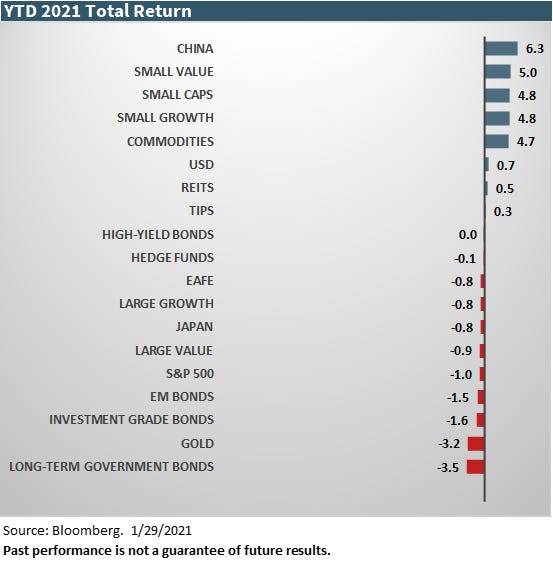

In the month ending January 29, 2021, the S&P 500 Index returned -1.02%, and the Bloomberg Barclays U.S. Aggregate Bond Index returned -0.72%. Year-to-date performance by asset class is shown below.

Click here to access RiskBridge Advisors’ 2021 Investment Outlook.

Follow on Twitter @risk_report