Looking Back at 2021

2021 In Review

As we close out the year, we look back at what we published this time last year as an investment analysis post-mortem. This annual exercise mainly focuses on what we got wrong, as we believe we learn more from our mistakes.

The immortal John Madden may have said it best, "Self-praise is for losers. Be a winner. Stand for something. Always have class and be humble."

We entered 2021 with a "wall of worry" that included (1) self-destructive political and social unrest in the US, (2) expanding income and wealth inequality, (3) runaway budget deficits and government debt, and (4) subdued consumer confidence with an unemployment rate at 6.7%.

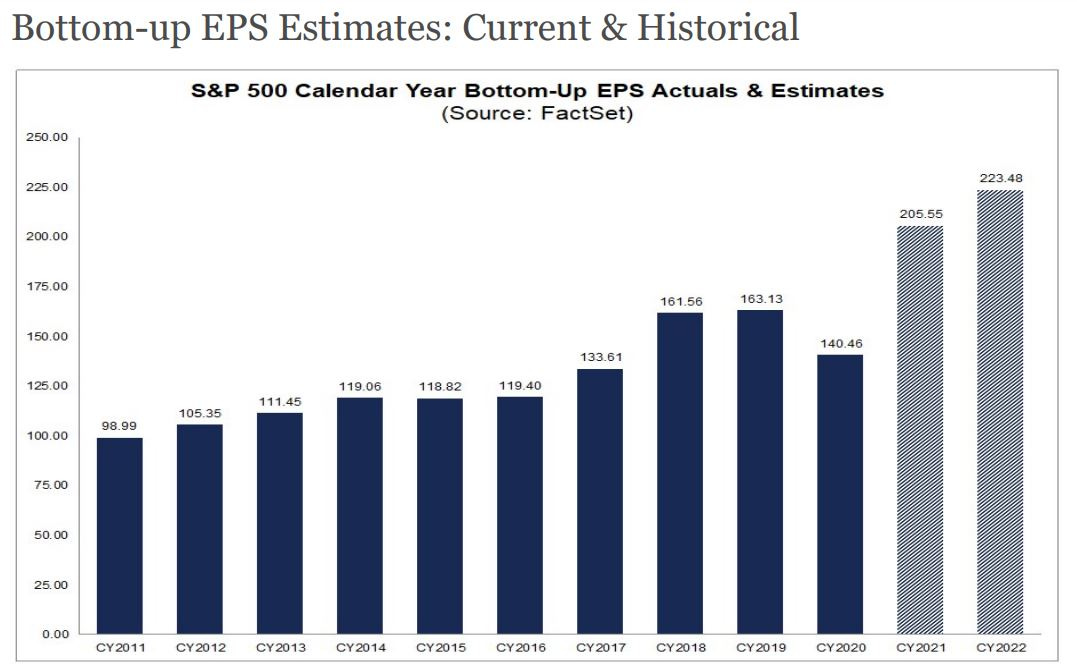

In hindsight, the opening of the global economy, aggressive monetary and fiscal stimulus, and corporate earnings growth of 46% y/y offered stronger-than-expected investment tailwinds throughout the year.

Here are a few excerpts from RiskBridge's 2021 Investment Outlook:

What we got wrong

"US GDP is projected to increase by 4.1% in 2021…" Bloomberg projects 2021 US real GDP growth to be 5.6%.

"However, after two years of outsized returns and current extreme valuations, we expect more muted asset returns in 2021." The S&P 500 Total Return Index rallied 29% in 2021 compared to its long-term annualized return of 10.2% (1990-2020).

"We expect a distressed commercial real estate cycle…." It hasn't materialized (yet).

"It appears the third big dollar rally since the end of Bretton Woods is over." US dollar index rallied +6% in 2021.

"Historically value outperforms growth when inflation is accelerating." In a year when CPI spiked to 6.8%, value underperformed growth by 349 basis points.

"We recommend being overweight non-U.S. equities, where relatively higher risk premia offer potentially higher future returns than US equities." MSCI ACWI (ex-US) returned 8%, underperforming the 29% return for US stocks.

"We recommend…emerging market debt." Bloomberg Emerging Market USD Debt Index returned -2%.

What we got right

"We believe 2021 offers hope for a brighter future. With the worst avoided, most of the global economy has been preserved and could revive quickly, in our opinion."

"We believe accelerating growth and inflation should continue to favor risk assets."

"Our analysis suggests that the yield on the 10-year Treasury note could trade as high as 2.0%. Under that scenario, Treasurys could be the worst performing assets class this year." The yield on the 10-year Treasury note missed the 2% mark, peaking at 1.74%, but the Bloomberg Long Term Treasury Index returned -5%.

"A reflationary regime that is bearish for Treasury securities and the dollar, but bullish for commodities, hard assets, and select equities." Wrong on the dollar call, but directionally right on the rest.

"A shifting volatility regime with interest rate vol rising and equity vol declining." For 2021, the MOVE Index (a proxy for interest rate volatility) is +59%, and the VIX Index (a proxy for equity volatility) is -25%.

Interest rate volatility was the best-performing segment (+59%). Equity volatility was the worst performer (-25%).

By asset segment, commodities (+41%), small-cap value (+29%) and large cap growth (29%) were the best performers. Laggards included the VIX (-25%), China (-21%), long-term government bonds (-5%), and gold (-5%). By equity sector, energy (+55%), real estate (+46%), technology (+36%) and financials (+36%) outperformed. Laggards included staples (17%), utilities (17%), communications (18%) and industrials (22%).

After steepening during the first half of 2021, the yield curve (10yr-2yr) finished the year where it started (79 bps).

The US dollar appreciated 6% against a basket of developed currencies, reversing its declining trend in 2020. Dollar strength in 2021 was especially harmful to USD investors allocating to emerging markets. The JP Morgan, Emerging Market Currency Index fell (-9%), the Bloomberg EM USD Aggregate Bond Index (-2%), MSCI China Index (-24%), and MSCI Brazil Index (-19%). Bright spots include MSCI India Index (+25%) and MSCI Russia (+20%).

Typically, commodities are negatively correlated to the dollar, meaning commodity prices fall when the dollar rises. 2021 was atypical. A stronger dollar was accompanied by rising commodity prices, with the S&P GSCI Total Return Index (+41%) and crude oil (+60%). Gold (-5%) and Bitcoin (+63%) provided fuel for many speculators to go for broke in crypto land.

Conclusion

Looking back on 2021, we believe the one constant was the value of good risk management. A well-designed, risk-based allocation strategy charted a disciplined path that kept investors on course. No matter what markets serve up in 2022, we believe it is essential for investors to remain focused on the two things they can control: the quantity of risk and the types of risk allowed into a portfolio.

DISCLOSURE:

Past performance is no guarantee of future results. Personnel of RiskBridge Advisors, LLC ("RiskBridge") prepared the Risk Report. The views expressed herein do not constitute research, investment advice, or trade recommendations. RiskBridge may, from time to time, participate or invest in transactions with issuers of securities that participate in the markets referred to herein, perform services for or solicit business from such issuers, and/or have a position or effect transactions in the securities or derivatives thereof.

This Risk Report is distributed for informational purposes only. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed, and RiskBridge makes no representation as to its accuracy or completeness. Any opinions, recommendations, and assumptions included in this material are based upon current market conditions, reflect the judgment of RiskBridge as of the date indicated, and are subject to change without notice. You acknowledge and agree that RiskBridge is under no obligation to provide any additional information or update such information in making the information available. Securities and/or indices highlighted or discussed in this communication are mentioned for illustrative purposes only and should not be construed as investment recommendations. All investments involve risk, including the loss of principal. Before implementing any strategy, be sure to consult with a qualified financial adviser and/or tax professional. Risk Report and this information are not intended to provide investment, tax, or legal advice, and this material is not to be relied upon in substitution for the exercise of independent judgment. This Risk Report is not to be reproduced, in whole or part, without the written consent of RiskBridge.